Fact Gate

Review Dates For Time-Sensitive Claims

- Reviewed on

- 2026-05-05, against the public references named in this article where external facts are used.

- Next review due

- 2026-05-31, or sooner if freight, tariff, market availability or public-source conditions change.

- Maintenance rule

- Update or remove time-sensitive wording before reuse if the linked sources no longer support it.

Answer Card

Buyer Decision Summary

- Problem

- In Gulf markets, Chinese vehicle growth is now turning into aftermarket pressure because many 2023 and 2024 sales are entering the first 18 to 24 month repair cycle.

- Best control

- Build a first basket around repeat service parts, then release visual or version-risk parts only with photo proof.

- Best buyer fit

- GCC / Middle East parts shops, workshops, distributors, and online sellers

- Brace support

- Jordan checks OE / VIN / old-part photos, confirms stock or source options, and routes mixed-order quotes to WhatsApp.

- Next step

- Send OE / VIN / photo on WhatsApp

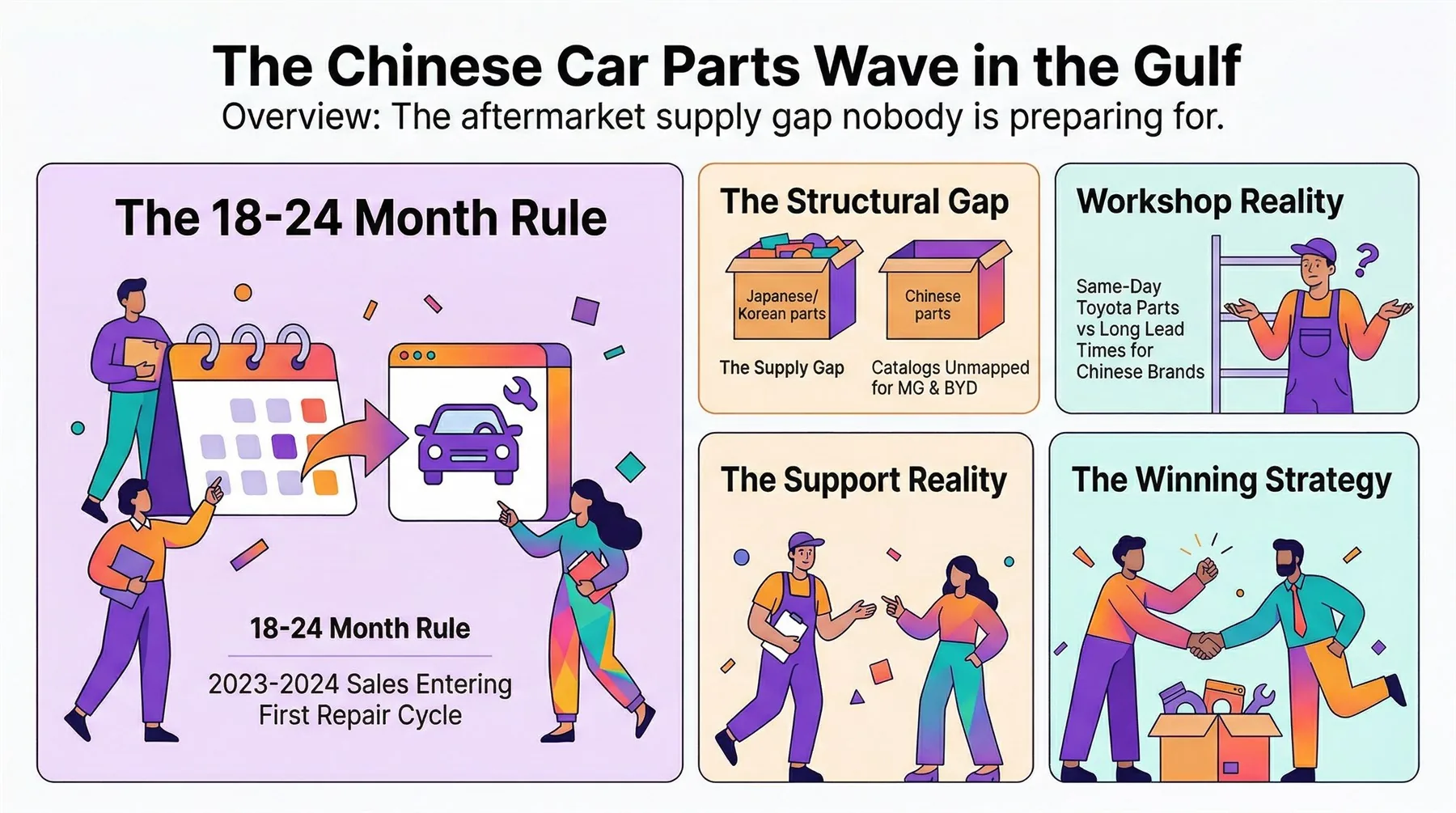

What Is the 18-to-24 Month Aftermarket Rule?

The 18-to-24 month aftermarket rule is the observed delay between new-vehicle delivery and the first meaningful wave of parts demand in repair channels. New cars do not generate aftermarket volume immediately. Most common repair scenarios — routine maintenance, minor collision, cooling stress, and electrical wear — only become visible once a vehicle has accumulated real-world mileage and environmental exposure. For Gulf markets, where heat, dust, and long-distance driving accelerate wear, this timeline can compress slightly, but the core pattern holds: vehicle presence precedes parts demand by roughly one and a half to two years.

Why Does The 18 To 24 Month Rule Matter?

New-car sales do not become aftermarket demand on day one. There is a delay between vehicle delivery and the moment parts demand becomes visible in repair channels. That delay is often around 18 to 24 months for many common repair scenarios. Once the first wave reaches workshops, the market stops asking whether the brand will matter and starts asking where the parts are.

That is why recent Chinese-brand sales in the Gulf matter now. The vehicles are already on the road, and the first meaningful repair cycle is beginning to expose whether local parts systems have kept up. In 2024, Chinese OEMs held over 70% share of new-vehicle sales growth in the Middle East. Those vehicles are now entering the exact window where bumper, lamp, mirror, and cooling-part demand becomes operational rather than theoretical.

The Numbers Behind the Gulf Shift

The GCC automotive aftermarket was valued at USD 11.7 billion in 2024 and is forecast to reach USD 17.3 billion by 2032, growing at a CAGR of 5.0% according to GMI Research. Within that expansion, the Chinese-brand segment is the fastest-growing slice because it started from near-zero share only a few years ago. In the UAE, a 2024 YouGov study found that 76% of consumers could name at least one emerging car brand, with Jetour at 42% awareness and BYD at 40%.

This is not a niche story. It is a structural reordering of the Gulf vehicle fleet. When fleet composition shifts, the aftermarket must follow. The table below shows how the market signals line up.

| Market Signal | What It Means | Operational Result |

|---|---|---|

| Rising Chinese-brand sales | More vehicles entering service population | Future collision and maintenance demand increases |

| 18-24 month repair cycle | First meaningful aftermarket wave begins | Parts shortages become visible to workshops |

| Catalogs still catching up | Local systems are incomplete | Fitment and sourcing take longer |

| Heat and dust exposure | Cooling and filtration parts wear faster | Radiator, condenser, and fan assembly demand rises early |

| Insurance workflow pressure | Collision claims need same-day parts | Body-part availability becomes a competitive advantage |

What Is The Structural Gap?

The structural gap is simple: vehicle presence has grown faster than parts support. Traditional systems already understand Toyota, Nissan, Hyundai, and other long-established nameplates. Their parts codes, local stock behavior, and repair expectations are familiar. Chinese brands are newer in many Gulf repair channels, so the support model is still catching up.

That means catalog logic can still be incomplete, common-moving items may not be stocked locally, and workshops may not know which supplier can actually handle mixed aftermarket demand across MG, BYD, GWM, Jetour, and similar brands. In 2025, Chinese vehicle exports shattered the 7 million mark for the first time, with the Middle East as a primary destination. The upstream supply chain is robust. The downstream aftermarket chain — catalog coverage, local stock, and fitment verification — is what lags.

Traditional Support vs. Chinese-Brand Support: A Comparison

Workshops in the Gulf do not struggle with Japanese or Korean brands because the support ecosystem matured over decades. For Chinese brands, the same ecosystem is still forming. The differences are not about part quality. They are about availability speed, catalog clarity, and supplier familiarity.

| Factor | Established Japanese/Korean Brands | Chinese Brands (MG, BYD, GWM, Jetour) |

|---|---|---|

| Catalog coverage | Nearly complete; local stock predictable | Partial; some models lack full part-code mapping |

| Same-day availability | Common for fast-moving items | Rare; often requires international sourcing |

| Workshop familiarity | High; most mechanics trained on these platforms | Low; fitment questions are frequent |

| Insurance workflow integration | Smooth; standard estimating systems cover most parts | Friction; non-standard parts can delay claims |

| Price range for common collision parts | USD 180-450 for bumpers; USD 90-220 for lamps | USD 120-320 for bumpers; USD 70-180 for lamps |

Why Are Workshops Feeling It First?

Workshops feel the gap before importers talk about it publicly because repair bays cannot wait for market narratives. When a vehicle needs a bumper, headlamp, mirror, condenser, or fan assembly, the workshop needs an answer on fitment and delivery. Delays immediately affect repair scheduling, customer updates, and insurance workflows.

The pressure is most acute in Sharjah and Dubai, where workshop density is high and customer expectations for turnaround time are aggressive. A workshop that can source a Toyota Corolla bumper in four hours may need four days for a GWM Cannon equivalent — not because the part is rare, but because the local supplier network has not yet built the same inventory depth.

Which Models Are Driving the Wave?

Not all Chinese brands are creating equal aftermarket pressure. The models with the highest sales volume in 2023-2024 are the ones now entering repair cycles. Based on registration and sales data from Gulf markets, the following model families are generating the most visible parts demand:

- MG ZS / HS / MG5 — High fleet penetration in rental and ride-hailing; collision and brake wear are early movers.

- BYD Atto 3 / Dolphin — Growing private ownership; cooling system and electrical parts are emerging categories.

- GWM Haval H6 / Jolion / Cannon — Strong in Saudi Arabia and Oman; body parts and suspension components lead demand.

- Jetour X70 / Dashing / T2 — Rapid growth in UAE and Qatar; lamp and mirror replacement is already visible.

- GAC GS3 / GS4 / GS8 — Smaller volume but rising; bumper and grille demand is increasing.

Importers who track these model clusters early gain a timing advantage. The workshop that has already sourced a Jetour Dashing headlamp once is the workshop that will order it again — and recommend the same supplier to competitors.

How to Build a Chinese-Brand Parts Support Chain

The winning strategy is not to pretend Chinese-brand demand is still niche. It is to build a working support loop early. Here is a practical framework for importers and workshop owners:

- Identify the top three models in your catchment area. Use registration data, workshop observation, or insurance claim patterns. Do not guess — focus on what is already on your lifts.

- Separate fast-moving from slow-moving categories. Body parts, lamps, mirrors, radiators, and condensers usually move first. Trim, interior, and electronic modules can wait.

- Map OE numbers for those categories. Even if you source aftermarket, knowing the OE reference reduces fitment errors and speeds up quoting.

- Find a supplier who can verify fitment with photos or sample checks. Catalog matching for Chinese brands is less mature than for Japanese brands. Visual confirmation reduces return rates.

- Start with a small test order. A first shipment of USD 2,000-3,500 covering 8-12 fast-moving lines is enough to test quality, delivery speed, and packaging.

- Track which lines move in the first 90 days. Use this data to refine your second order. The first 90 days teach more than any market forecast.

- Build a relationship, not a transaction list. A supplier who understands your model mix and delivery expectations will prioritize your orders when stock is tight.

- Share feedback on fitment and quality. Chinese-brand aftermarket catalogs improve fastest when suppliers receive specific, actionable feedback from the field.

For Gulf buyers, the strongest partners are the ones who can handle urgency, mixed-brand requests, and real availability checks without turning every inquiry into a catalogue search exercise.

Sources & Methodology

This article combines public market data with industry pattern observation. The GCC aftermarket size and growth forecast (USD 11.7 billion in 2024, CAGR 5.0%) comes from GMI Research. UAE consumer brand awareness figures (76% recognition, Jetour 42%, BYD 40%) are from a 2024 YouGov survey. Chinese export volume data (7 million units in 2025) is reported by Gasgoo based on industry statistics. The 18-to-24 month aftermarket rule is an industry-observed pattern, not a formal published study, but it is widely referenced in aftermarket strategy discussions. Price ranges for collision parts are estimated based on public aftermarket catalog listings and do not represent Brace Auto Parts pricing. All non-public claims — specific workshop experiences, supplier behavior, and operational recommendations — are based on the author's direct observation in the Chinese auto parts export market.

FAQ

Why now, not later?

Because the first large wave of Chinese-brand vehicles is already reaching the repair cycle where parts demand becomes visible.

Which parts usually show the gap first?

Collision body parts, lamps, mirrors, condensers, and fan assemblies often show the support gap first.

Is the problem demand or execution?

Demand is already present. The real challenge is execution, fitment clarity, and inventory support.

What should importers do first?

Track fast-moving models, common repair items, and suppliers who can verify fitment quickly for GCC workflows.

Are Chinese-brand parts cheaper than Japanese-brand equivalents?

Aftermarket collision parts for Chinese brands typically cost 20-35% less than equivalent Japanese-brand aftermarket parts, but pricing varies by supplier, volume, and shipping terms.

Buyer Downloads

Use This Guide In A Real RFQ

RFQ Template

Copy This RFQ Format

Brand / model: Year: OE number: VIN: Old part photo: Quantity: Destination: Need photo confirmation before shipment? Yes / No